अर्थसंकट का भूत हमीं के कंधे वेताल

कर्ज खाये कंपनियां

ब्याज चुकाये हम

कालाधन उनका फिर फिर

शामिल अर्थ दुश्चक्र में

उन्हीं के हवामहल में कैद

हमारे ख्वाब तमाम

पलाश विश्वास

Corporate India has gone on a foreign currency loan binge. Result? The external debt of corporates, or debt denominated in a foreign currency, has increased from $118 billion in fiscal year 2009 to $224 billion in fiscal year 2013.

अजब देश की गजब कथा है साधो

हमींपर मेहरबान सावन भादो

संकट के सारे मानून हमीं पर बरसे

खेती खत्म तो मरे हम थोक भाव

उत्पादन ठप तो भी मरे हम

अमेरिका में आ जाये मंदी

तो आफत हमारी वह

अमेरिका मंदी से उबरे

तो वह आफत भी हमारी

अर्थसंकट का भूत हमीं के कंधे वेताल

कर्ज खाये कंपनियां

ब्याज चुकाये हम

कालाधन उनका फिर फिर

शामिल अर्थ दुश्चक्र में

उन्हीं के हवामहल में कैद

हमारे ख्वाब तमाम

अब तो सबूत भी हाथों में है साधो

देश बेचने वाले

किसकी भर रहे हैं जेबें

और किन पर हैं तमम बैंक मेहरबान

किनके लिए यह प्रत्यक्ष विदेशी पूंजी निवेश

किसके मुनाफे खातिर रोज

बदलता जाता कानून

निवेशकों की आस्था गिरने का

झूठ हुआ है बेनकाब साधो

यकीन न हो तो पढ़ लो

इकानामिक टाइम्स साधो

यही तो बता रहे हैं हम अरसे से साधो

वित्तीय नीति कोई नहीं है

करारोपण असमर्थ हमारे विरुद्ध

अब प्रत्यक्ष कर प्रणाली भी

दे रही दस्तक दरवाजे पर

मुद्रास्फीति,मंहगाई और जनादेश

प्रबंधन की मजबूरियां हैं

राजनीतिक बाध्यताएं हैं

चुनौती देती अस्मिताएं हैं

बस,इसीलिए

हवा में ही स्थगित है

निर्णाय वार

वध्यभूमि में लेकिन

वध को प्रस्तुत हम तैयार

धीमा है आर्थिक सुधार

कारपोरेट नीति निर्धारण की कोई विकलांगता

जैसी चीज होती ही नहीं कहीं

राडिया टेप को बांच लेना साधो

हर बार मरता है लेकिन माधो

हमने कितनी बार कहा है,लिक्खा कितनी बार

कालजयी कवि लेकिन दुहराते नहीं कथा बारंबार

भालुओं और सांड़ों का आईपीएल हमारा नहीं

चियरिनों का यह कार्निवाल भी हमारा नहीं

अनंत मनुस्मृति व्यवस्था है उत्तरआधुनिक

अनंत क्रयशक्ति संपन्न जाति वर्चस्व है उत्तरआधुनिक

अनंत वैचारिक विश्वासघात है उत्तरआधुनिक

पूंजी में ही निष्णात है यह लोक गणराज्य

पूंजी का हित ही साधता यह लोकतंत्र

प्राकृतिक संपदा न हमारी हुई

और न राष्ट्र का हुआ कभी

उसपर कारपोरेट पताका फहराया

हमें करते रहे बेदखल

खनिज न हमारा हुआ

न राष्ट्र का हुआ खनिज

नियमागिरि पर झंडा लहराया

आदिवासी भूगोल को माओवादी ठहराया

हमारे हिस्से में है मुद्रास्फीति

मंहगाई का बोझ

हमारे हिस्से में है विकास दर

निरंतर घटती हुई

हमारे हिस्से में है

वित्तीयघाटा बढ़ता हुआ

हमारे हिस्से में है भुगतान असंतुलन

हमारे हिस्से में है 1991 का ईश्वर

और सुनामियों का समय यह

बाढ़ भूस्खलन और भूकंप का समय यह

युद्ध और गृहयुद्ध का समय यह

हमारे हिस्से में है

सशस्त्र सैन्यबल अधिनियम

और हमरे हिस्से में है नाना किस्म का

सलवाजुड़ुम राष्ट्रव्यापी साधो

हमारे हिस्से में है खंडित यह देश

प्रचंडतम धर्मोन्मादी आत्मघात साधो

कारपोरेट से बड़ा

धर्म निरपेक्ष कोई नहीं साधो

अमेरिकी इजराइली हित

कैसे सधते देखो साधो

पूंजी कहां से आती है

पूंजी कहां से खप जाती है

निवेश कहां होता है

विनिवेश कहां होता है

रुपया क्यों गिरता है

रुपया उठता भी है क्यों

शेयर बाजार के खेल में

अरबों का न्यारा वारा

दांव हमारा है साधो

जीत उन्हीकी है साधो

मौद्रिक कवायद उन्हीके लिए साधो

Editor's Pick

Reliance Power Ltd.

BSE

68.70

-0.40(-0.58%)

Vol: 2589962 shares traded

NSE

68.75

-0.35(-0.51%)

Vol: 7351674 shares traded

Prices | Financials | Company Info | Reports

India Inc sitting on debt bomb: Why the health of large corporates should worry us all

G Seetharaman

Earlier this week, the director of the Central Bureau of Investigation Ranjit Sinha warned that the agency may begin a probe into the rising volume of loan defaults, and look into the possible culpability of senior officials of mainly public sector banks.

Pointing to the fact that non-performing assets (NPAs) of public sector banks had risen by 95% between 2010 and 2012, he made the additional point that the bulk of NPAs were from the top 30 defaulters for most public sector banks.

Former Reserve Bank of India (RBI) governor C Rangarajan, who was present at the event in Delhi where Sinha made those comments, differed pointing to the fact that NPA levels are also due to the weak state of the economy.

"Every NPA is not due to motivated actions of bank employees," he is reported to have said. Much of the weakness in the economy, and the recent crash in the rupee and stocks, has been blamed on the failure of the current government to carry out structural reforms.

The weak economy is certainly an important part of the large and growing NPA problem. But even the RBI itself doesn't seem to think that's the only story.

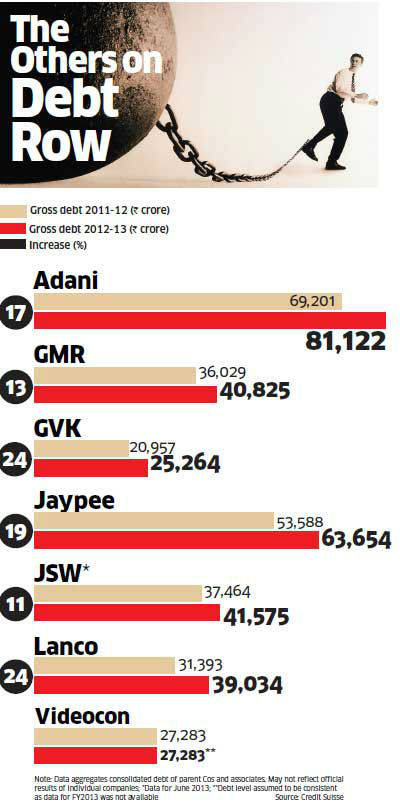

In other words, the Indian banking system — and this is to a considerable extent the problem of public sector banks — is heavily exposed to the fortunes of just these groups. The report, an updated version of a similar one published last year, points to worrying trends.

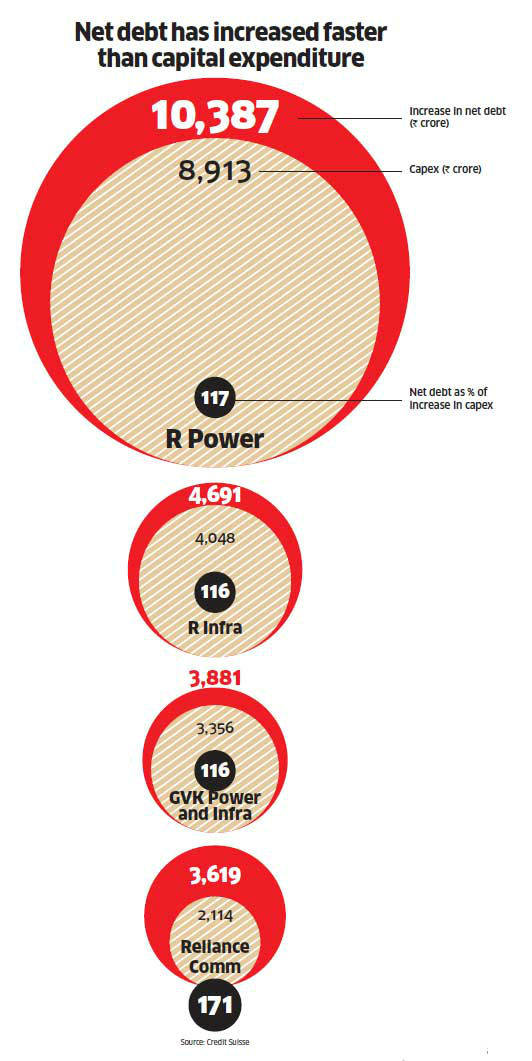

One, the collective debt levels of these groups have actually risen from last year by 15%. Secondly, their ability to service this debt has deteriorated.

"The largest increases have been at groups such as GVK, Lanco and ADA where the gross debt levels are up 24% year on year. For most of these corporate groups, the debt increase even outpaced capital expenditure. Asset sales — key for deleveraging for most of these — have still not taken-off; only GMRand Videocon have had some success on that front," says the report.

The groups for their part punch holes in theCredit Suisse report. A Reliance ADA Group spokesperson argues that "a figure of gross debt without reference to the break-up and the purpose for which it has been incurred is quite meaningless and altogether misleading."

He adds: "Our levels of debt are more than reasonable and commensurate looking at the scale and magnitude of the projects we are developing, and their assured high-quality revenues... The increase in debt from fiscal years 2012 to 2013 is a natural consequence of debt being drawn down for capex as our various projects have moved towards completion."

* * |

An Essar spokesperson says: "Each individual asset ties up its own financing as per their capital requirement which comes with varying terms and maturity profile. Therefore consolidation of debt of individual companies to arrive at gross debt and repayment could be misrepresentative."

* * |

Vedanta claims its outstanding debt is at Rs 93,068 crore, about Rs 6,500 crore less than the figure in the report. Groups such as GMR, GVK, Adani, JSW, and Lanco did not respond to questionnaires sent by ET Magazine. A spokesperson for Jaypee said that, "you should not take data from any other source except from our...audited and published results."

To be sure, the ability to service those increased debt levels does vary widely across such groups. Vedanta, for instance, raked in gross profits well in excess of the interest payments it had to make in 2012-13. In comparison, groups like Lanco, GMR and GVK did not earn enough in profits to make interest payments.

It's not just the top 10 corporate groups. According to the Morgan Stanley report, the ability of the BSE-500 companies to earn enough in gross profits to pay interest is at its lowest level in the past decade, and is approaching the levels of the late '90s.

One view is that overleverage among companies, and deterioration in the ability to pay interest, are a standard feature of cyclical downturns. As Saurabh Mukherjea, chief executive of institutional equities at Ambit Capital argues: "There is nothing spectacularly surprising about corporates with huge debt in a downturn. It's a fairly prosaic feature of economic cycles so why develop a morbid fascination with the laggards? Some might even go bankrupt but there is plenty of money to be made by investing in companies with strong fundamentals."

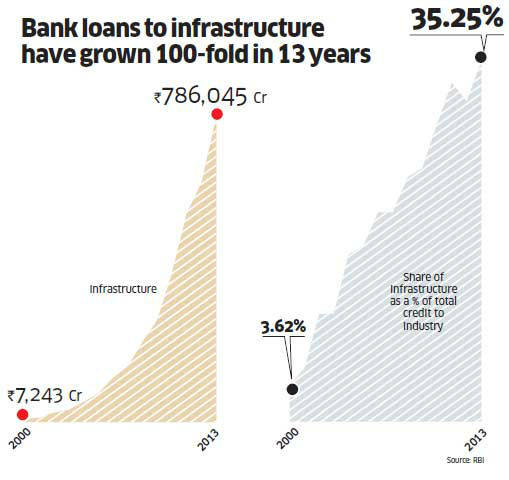

But from the perspective of corporate debt there is one stark difference that stands out, in this downturn, as compared to the earlier downturn era of the late '90s and early 2000s — the predominance of infrastructure.

* * |

The Infra Story

In 1999, there were three sectors which dominated bank credit to industry — engineering (12% of total loans to industry), chemicals, dyes and paints (around 11%), and a large residual 'other' which accounted for around 20% of loans. Since the early 2000s, however, there has been one industry which has arguably dominated bank lending — infrastructure. It now accounts for 35% of all bank credit to industry, dwarfing all other sectors; no other area of business comes even close.

It's no accident then that among the list of top business houses and their levels of leverage, the infrastructure business, especially power, dominates. What are the implications of such a heavy concentration of bank lending to just one sector? Since an individual loan to an infrastructure project can run into the few hundred or even thousand crores, basic lending norms had to be tweaked to facilitate such loans.

Over the years, the RBI relaxed norms relating to the amount of loan that could be given to a single borrower or group, it allowed banks to finance promoter's equity, and it relaxed the types of collateral required for such projects. It further relaxed the conditions under which such loans could be restructured when they ran into difficulties of repayment. Infrastructure companies tend to have much higher leverage than other industries. None of this was necessarily a bad thing — quite the opposite.

Without such norms being relaxed it was unlikely that the funding necessary for suchinvestments would have been forthcoming, and infrastructure assets have been built. "Though there may be some haircut [losses from bad loans] on the portfolio for the banking sector, one can draw comfort from the fact that at least some assets have been created," RBI's Chakrabarty points out.

"The need of the hour for the Central government, state governments and the project developers is to ensure that the minor impediments that ail the operationalisation of these assets are immediately removed so that they can be put to productive use and start generating revenues."

This is what the borrowers themselves are looking forward to. "We are at an investment cycle where the majority of our investments have been completed or are nearing completion; accordingly earnings from these projects will accrue once the projects are fully operational," says an Essar spokesperson.

"Therefore we will see a significant uptick in revenue and profitability in the next two years as these projects begin to deliver." "Given the state of the economy, there is stress across sectors and across, small, mid and large corporates," says MS Raghavan, chairman and managing director of IDBI Bank. "But, it has not reached unmanageable levels. In fact I think the stress will taper off from now because of efforts being made by various government agencies. For instance, an inter-ministerial group has cleared 28 infrastructure projects."

Options

There's a fundamental reason why the health of such large groups should worry us all. In a sense, because of their size, and their importance in the banking system and the infrastructure sector, weak fundamentals of these groups will seriously affect the ability ofIndia Inc as a whole to start investing again. "Some of the infrastructure developers now have debt, which is 20-25 times their market cap," says Morgan Stanley. "Will these corporates have the ability to borrow to start new projects? Unlikely, in our view."

Unfortunately, the debt of such groups has now reached a size where they have the potential to affect the health of a large number of banks, and the ability of India Inc as a whole to weather the recovery and emerge in investing mode. So what are the options facing such groups? In Vedanta's case, the strategy is straightforward. "Majority of the debt is planned to be repaid from free cash flow from operations and is expected to reduce the leverage going forward," a company spokesperson said.

The Reliance ADA Group too expects cash to begin flowing in. A company spokesperson says that eight of 11 road projects are now operational "The Sasan ultra mega power project was recently commissioned and the first turbine and the remaining turbines are scheduled to be commissioned this year; the Rosa power project is now fully commissioned; our Mumbai Metro project is on track to be commissioned later this year, and so on."

Another way is to replace high cost with lower-cost debt. At the Essar group, for instance, companies such as Essar Steel and Essar Oil are looking to collectively raise $7.7 billion in dollar loans. "Various businesses are in the process of replacing the high cost rupee debt with dollars," says an Essar spokesperson. "Considering that the earnings of these businesses are either dollar denominated or dollar linked, there is a natural hedge against volatility in the exchange rate."

Asset sales are a third option. In June, Videocon sold a 10% stake in a Mozambique gas field to a consortium of ONGC Videsh and OIL India. "We will be getting about Rs 16,000 crore from the Mozambique stake sale. With that, we will repay about Rs 12,000 crore of domestic debt by the end of September," says Venugopal Dhoot, chairman and managing director of Videocon.

That leaves the group, says Dhoot, with about Rs 7,000 crore of domestic debt and Rs 8,000 crore of overseas debt which has been taken against foreign assets and will be paid over time. "I don't see any reason to sell our assets now," he says. Companies such as GMRare reported to have been in talks over the past several months to sell bits of its road assets portfolio.

But even in such cases, companies are often running to simply stand still. Despite sales of assets such as GMR Jadcherla Expressways and Island Power, which have actually gone through, GMR infra's debt levels have increased by 13% in 2012-13. Groups are also rejigging entire projects. Essar is converting two gas plants to thermal plants, following the gas shortages in the power sector. It expects the economics of its Mahan plant in Madhya Pradesh to improve once it gets its clearances in place for its coal block, which, the spokesperson says, should come through in a few months.

Finally, like other power producers hit by shortages of domestic coal and high prices of international coal, it has approached regulators asking for approval to raise tariffs for end-consumers. But it's almost certain that banks will have to write off some amount of these loans they made against their capital. And given that the pain will be felt largely by public sector banks, many will likely end the current downturn with a severely depleted capital base; this in turn will require infusions of capital from the government, and ultimately, the taxpayer.

More from The Economic Times

Infosys loses another senior executive in Sudhir Chaturvedi 24 Aug 2013

Finance Ministry all ears as banks line up plans to boost forex inflows 25 Aug 2013

Non-performing assets force banks to woo small cos 10 Aug 2013

SBI: Focus on retail to help in times of slowdown 13 Aug 2013

* * |

In power, the big stumbling block in recent years has been coal shortages which lead to many projects being delayed or running at well below the capacity needed to earn adequate revenues to service debt.

Recent reforms though have allowed thermal plants to pass on the greater fuel costs to endconsumers and recover fixed costs.

"While this has not happened with retrospective effect [enabling plants to recoup losses made in earlier years], this is still hugely positive," says Ashok Khurana, director general of the Independent Power Producers' Association of India (IPPAI).

"This move will go a considerable way in alleviating the bad-loan problem facing power producers." Indeed one of the key criticisms of the UPA government is that it was going too slow on implementing exactly such reforms which would get infrastructure moving and projects underway, thereby enabling banks to get their money back.

Sting in the Tail

But it's not that simple. Even if policy reforms get moving, and projects start delivering and raising revenues, analysts point to one elementary fact: currently, given that a large number of projects are in the construction phase, interest on the debt raised for such projects is 'capitalised'.

Put simply, because the project is not yet operational and raising revenues to pay off loans, the interest accrued so far is added to the cost of the project and reflected on the balance sheet, rather than being paid off through the profit and loss account. As and when the project starts generating cash that interest moves off the balance sheet and starts getting charged to profits.

"With capitalised interest currently at 30-250% higher than the [interest currently paid out of profits], the interest burden may also sharply rise as projects come on stream," points out theCredit Suisse report. For Reliance Power, for instance (which will see a large amount of capacity coming online this year), interest paid out of gross profits is currently Rs 585 crore. Its capitalised interest is Rs 1,465 crore. In GVK Power's case, 'expensed interest' is Rs 707.9 crore. Capitalised interest is Rs 1,067 crore.

"On infrastructure loans, we have started seeing some restructurings [of loans] in the past two quarters. However, the big jump is likely to happen over the next two years as more loans come up for cash payment [large part of loans are still in the construction phase]," saysMorgan Stanley. Indeed, so far NPAs in banking have reflected weakness in other sectors — agriculture, and small and medium corporates. Soon though, NPAs will start reflecting those multi-thousand crore infrastructure assets as well.

* * |

In a speech recently on bank lending to the infrastructure sector, which now accounts for 35% of total loans to industry, deputy governor KC Chakrabarty stated: "I reiterate that the reason for NPAs is non-performing administration.

In the case of infrastructure, this could also be on account of non-performance beyond that of the bank management — that of policymakers, bureaucracy etc.

But what is really puzzling is why this affects the public sector banks the most...The answer lies squarely in the poor project appraisal techniques, lack of accountability, post-disbursal supervision, etc.

In our assessment, the project appraisal and the decision making in public sector banks has been more impressionistic rather than being information based.

How else does one defend the eagerness of some banks to fund power distribution companies with negative net worth!"

"The huge leverage of Indian infrastructure companies is a combination of their over-willingness to take on projects and poor lending standards of banks," points out Nick Paulson-Ellis, chief executive of Espirito Santo Securities India.

"Private banks are much more prudent in their lending than state-owned banks," he adds. "Over the past few years, loan growth has been driven by a few levered corporates, initially leveraging up the balance sheet and later rolling over — the balance sheets at some of these corporates are stretched," a report by Morgan Stanley pointed out.

What are the consequences of such high levels of leverage, and what do they imply for the ability of corporate India to not just weather the downturn, but emerge from it leaner and stronger?

Fuelled by Debt

A recent report by Credit Suisse points to the scale of the problem in the context of large corporate houses.

According to the report, 10 corporate groups — the Adanis, Vedanta, GMRBSE 1.90 %, GVK and Jaypee among others — together account for around 13% of all banking system loans.

No comments:

Post a Comment